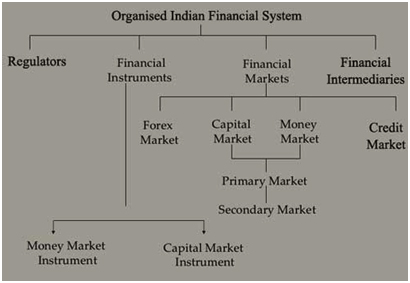

The financial system comprises a mixture of intermediaries, markets and instruments that are related to one another. It provides a system by which savings are transformed into investments.

The Reserve Bank of India (RBI) being the central banking authority, exercise monetary control and supervises the banking institutions. Different institutions such as Commercial Banks, Non Banking Finance Companies, Mutual Funds Insurance Companies, Primary Dealers, brokers, depositories and Insurance Agents, also different markets such as the capital market and the money market are part of the financial system.

The three regulatory authorities viz., RBI, SEBI, (Securities and Exchange Board of India, IRDA(Insurance Regulatory Development Authority), are controlling and supervising the banking, capital market and insurance sectors respectively.

Objectives of Financial Sector Reforms in India

India has had more than a decade of financial sector reforms during which there has been substantial transformation and liberalization of the whole Financial system. Following are the objectives of the reforms –

- Reforms Financial repression that existed earlier

- Create an efficient productive and profitable Financial sector industry

- Enable price discovery particularly by the market determination of interest rates that then helps in efficient allocation of resources

- Provide operational and function autonomy to institutions

- Prepare the Financial system for increasing international Competition

- Open the external sector in a calibrated fashion

Some Financial Institutions

Securities Exchange Board of India (SEBI): It is regulatory authority of stock exchanges and protects investors from fraudulent dealings. It was established in April 1988 and awarded statutory status by Act of parliament in 1992. SEBI Head quarters located in Mumbai.

Insurance Regulatory & Development Authority (IRDA): It is apex body formed under Sec.4 of IRDA Act 1999 to protect the interests of the policyholders to regulate promote and ensure orderly growth of the insurance industry in India

Indian Banks Association (IBA): It is the official association of all the banks operating in India. It acts as a bridge between banks on one hand and government and staff unions on the other.

Financial Stability & Development Council: This is the apex financial regulator of our country. Headed by Finance Minister, it coordinates and regulates to four financial regulators of the country i.e. RBI, SEBI, IRDA and PFRDA to ensure that all of them operate and function in harmony to promote the growth and stability of Indian Economy.

Non Banking Financial Company (NBFC): These are companies which have functions similar to banking like accepting deposits and making loans. However they do not have license for banking, although they are regulated by RBI.

Deposit Insurance & Credit Guarantee Corporation (DI&CGC): It is a wholly owned subsidiary of RBI which provides an insurance cover of Rs.1lakh per depositor per bank in case of bank failure. It also provides guarantee of repayment amount in default of small loans given by banks.

Export Credit Guarantee Corporation of India (ECGC): ECGC is a Govt. body which provides export credit insurance facilities to exporters and banks in India. It encourages Indian exporters by giving them credit insurance covers.

Banking Codes and Standards Board of India: It is an industry watch dog set up by RBI to monitor and assess the compliance with codes and minimum standards of service to individual customers, as prescribed by the RBI.

Credit Information Report: A Credit Information Report is a factual record of a borrower’s credit payment history compiled from information received from different credit grantors. Its purpose is to help credit grantors make informed lending decisions-quickly and objectively.

Credit Rating: Credit Rating is an assessment of the probability of default on payment of interest and principal on a debt instrument. In simple words, it ranks the company or country’s ability to meet their debt obligations.

Financial Markets:

A Financial Market can be defined as the market in which financial assets are created or transferred. As against a real transaction that involves exchange of money for real goods or services, a financial transaction involves creation or transfer of a financial asset. Financial Assets or Financial Instruments represents a claim to the payment of a sum of money sometime in the future and /or periodic payment in the form of interest or dividend.

Money Market- The money market is a wholesale debt market for low-risk, highly-liquid, short-term instrument. Funds are available in this market for periods ranging from a single day up to a year. This market is dominated mostly by government, banks and financial institutions.

Capital Market:

The Capital Market is designed to finance the long-term investments. The transactions taking place in this market will be for periods over a year.

Forex Market - The Forex Market deals with the multicurrency requirements, which are met by the exchange of currencies. Depending on the exchange rate that is applicable, the transfer of funds takes place in this market. This is one of the most developed and integrated market across the globe.

Credit Market- Credit market is a place where banks, FIs and NBFCs purvey short, medium and long-term loans to corporate and individuals.

Financial Intermediaries

Stock Exchange: A Stock Exchange provides a platform for sale and purchase of securities on behalf of the investors. They also provide clearing house facilities for getting of payment and delivery of securities. Clearing houses guarantee all payments and deliveries. Securities include equities, debt and derivatives.

Depositories: Depositories – There are two Central Depository Securities Ltd. (CDSL) and National Securities depositories Ltd. (NSDL) hold securities in demat form. Demat means conversion of physical securities into electronic form. The depositories transfer securities from sellers account to buyers account in electronic form up to instructions from the Stock Exchange Clearing House, supported by necessary documentation.

Financial Instruments

Equity and debt instruments:

Companies wishing to raise equity or debt through stock exchange have to approach a capital market regulator with the prescribed applications and a proforma prospectus for permission to raise equity and debt to get them listed on a stock exchange.

Mutual Funds:

A Mutual Fund is a form of collective investment that pools money from the investors and invests in stocks, Debt and other securities. It is a less risky investment option for an individual investor. Mutual funds require the regulators’ approval to start an Asset Management Company and each scheme has to be approved by the regulator before it is launched.

Call /Notice-Money Market

Call/Notice Money is the money borrowed or lent on demand for a very short period. When money is borrowed or lent for a day, it is known as Call (Overnight) Money. When money is borrowed or lent for more than a day and up to 14 days, it is "Notice Money". No collateral security is required to cover these transactions.

Treasury Bills: Treasury Bills are short term (up to one year) borrowing instruments of the union government. It is an IOU of the Government. It is a promise by the Government to pay a stated sum after expiry of the stated period from the date of issue

Certificate of Deposits

Certificates of Deposit (CDs) is a negotiable money market instrument and issued in dematerialised form or as a Usance Promissory Note, for funds deposited at a bank or other eligible financial institution for a specified time period.

CDs can be issued by (i) scheduled commercial banks excluding Regional Rural Banks (RRBs) and Local Area Banks (LABs); and (ii) select all-India Financial Institutions that have been permitted by RBI to raise short-term resources within the umbrella limit fixed by RBI.

Commercial Paper

CP is a note in evidence of the debt obligation of the issuer. On issuing commercial paper the debt obligation is transformed into an instrument. CP is thus an unsecured promissory note privately placed with investors at a discount rate to face value determined by market forces. The minimum maturity period of CP is 7 days. The minimum credit rating shall be P-2 of CRISIL or such equivalent rating by other agencies.

QUESTION AND ANSWERS

- Which of the following cannot be included in the definition of a ‘financial intermediary’?

A. Banks and non-bank finance company

B. Financial Institutions

C. Mutual Fund

D. Companies Engaged in Manufacturing of Goods

- Which of the following cannot be included in the money market?

a. Call or Notice Money

b. Corporate Securities

c. Certificate of Deposit

d. Treasury Bills

- Which of the following is a part of the money market?

A. Bonds issued by the govt.

B. Bonds issued by Public Undertaking

C. Term Money

D. Debentures

- The central bank in India is performing two distinct roles in the context of money market that includes:

A. Monetary control and banking supervision

B. Issue of currency and maintaining of CRR

C. Handing govt. business and maintaining price stability

D. Banking supervision and financial stability

- Money control is exercised by RBI in India through:

A. Payment System

B. Issue of Currency

C. Cash Reserves and Liquid Reserve Ratios

D. Repo Rate and Reserve Repo Rate

- The base rate for lending of banks is impacted by RBI by changing?

A. CRR

B. SLR

C. Repo rates and bank rate

D. Guidelines u/s 35A of B R Act

- Which of the following functions is not coming under functions of central banking authority in India?

A. Supervision over NBFC

B. Supervision over the Foreign Institutional Investors

C. Management of Financial Systems

D. Regulating the Money Market

- Which of the following is not the function of capital market regulatory authority i.e. SEBI, in India:

A. Regulating of Debt Market

B. Control over the Equity Market

C. Framing the Rules for Pension Funds

D. Supervision over Listed Companies

- Supervision over the depositors and stock exchanges is the role of?

A. RBI

B. IRDA

C. SEBI

D. PFRDA

- Which of the following does not match?

A. Regulator of Insurance Market----IRDA

B. Regulator of Capital Market ---SEBI

C. Regulator of Money Market ---RBI

D. Regulator of Forex Market---SEBI

- Which of the following functions is not carried by IRDA in India?

A. Regulator of Insurance Companies

B. Regulating the Insurance Products

C. Regulation over the Funds Managing Pension

D. Supervision of the General Insurance Market

- The small companies/ organizations that have been created exclusively to deal in govt. securities are called?

A. NBFCs

B. Mutual Funds

C. Primary Dealers

D. Asset Management Companies

- Which of the following have been created to provide long term funds for industry or agriculture?

A. Mutual Funds

B Financial Institutions

C. Asset Management Companies

D. Non-banking finance companies.

- Which of the following functions is not carried out by RBI?

A. Bankers to Govt.

B. Raising Deposits from Public

C. Lender of Last Resort to Banks

D. Management of Govt. Debt

- The clearing house facilities for payment and delivery of securities is provided

A.SEBI

B. Stock Exchange

C. Clearing Corporation of India

D. All the above

- The funds based outside India and authorised by SEBI to invest in Indian equity market through the stock exchange are called:

A. Foreign Institution Investors

B. Overseas Corporate Bodies

C. Non-resident Funds

D. Foreigner Investment Funds

- The corporate securities are held in electronic from instead of physical with?

A. Registrars

B. Custodians

C. Depositors

D. Mutual Funds

- Which of the following is the role of mutual funds?

A. To promote unit based scheme to inculcate saving habit

B. Pooling of investor money for investment in capital market and other securities

C. Manage the funds of high net worth individuals

d. All the above

- Which of the following is not a correct statement?

A. RBI exercises monetary control through CRR and SLR

B. Clearing house at various centers are maintained by SBI

C. IRDA is the regulator of insurance market

D. Rising of money through issue of shares by a company is part of capital market.

- Urban cooperative banks are controlled by:

A. NABARD

b. Central Govt. and NABARD

C. State Govt. and RBI

D. RBI and NABARD

Answers

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| D | B | C | A | C | C | B | C | C | D |

| 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 |

| C | C | B | B | B | A | C | B | B | C |

Download:

More Articles

Most Read