Sakshi Education

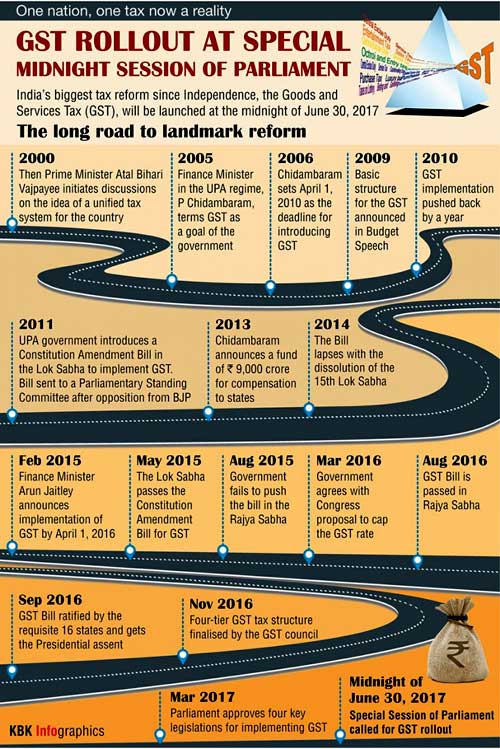

Goods and Services Tax (GST), India's biggest tax reform, was launched at midnight at Parliament's historic Central Hall, by President Pranab Mukherjee and Prime Minister Narendra Modi to change the indirect tax regime from 1st July. The introduction of Goods and Services Tax (GST) is a very significant step in the field of indirect tax reforms in India. By amalgamating a large number of Central and State taxes into a single tax, it would mitigate cascading or double taxation in a major way and pave the way for a common national market.

From the consumer point of view, the biggest advantage would be in terms of a reduction in the overall tax burden on goods, which is currently estimated to be around 25%-30%. Introduction of GST would also make Indian products competitive in the domestic and international markets.

Goods and Service Tax (GST) is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture up to final consumption with credit of taxes paid at previous stages available as setoff. In a nutshell, only value addition will be taxed and burden of tax is to be borne by the final consumer.

Constitution (101st Amendment) Act, 2016

The Constitution (122nd Amendment) Bill was introduced in the 16th Lok Sabha on 19 December, 2014. The Bill was passed by the Lok Sabha in May, 2015.

The Bill with certain amendments was finally passed in the Rajya Sabha and thereafter by Lok Sabha in August, 2016.

Further the bill had been ratified by required number of States and received assent of the President on 8th September, 2016 and has since been enacted as Constitution (101stAmendment) Act, 2016 w.e.f. 16th September, 2016.

The levy of the tax can commence only after the GST Law has been enacted by all the legislatures. Four Laws namely CGST Act, UTGST Act, IGST Act and GST (Compensation to States) Act have been passed by the Parliament and since been notified on 12th April, 2017. The States have passed SGST Act.

Changes to the Constitution

Article 246A of the Constitution, which was introduced by the Constitution (101st Amendment) Act, 2016 confers concurrent powers to both parliament and state legislatures to make laws with respect to GST.

Under Article 269A of the Constitution, the GST on supplies in the course of inter-State trade or commerce shall be levied and collected by the Government of India and such tax shall be apportioned between the Union and the States in the manner as may be provided by Parliament by law on the recommendations of the Goods and Services Tax Council.

Goods and Services Tax Council (GSTC):

The GSTC has been notified with effect from 12th September, 2016. GSTC is being assisted by a Secretariat.

A Goods and Services Tax Council (GSTC) shall be comprised by the Union Finance Minister, the Minister of State (Revenue) and the State Finance Ministers to recommend on the GST rate, exemption and thresholds, taxes to be subsumed and other features.

One half of the total number of members of GSTC would form quorum in meetings of GSTC.

Decision in GSTC would be taken by a majority of not less than three-fourth of weighted votes cast. Centre and minimum of 20 States would be required for majority because Centre would have one-third weightage of the total votes cast and all the States taken together would have two-third of weightage of the total votes cast.

The following major decisions have been taken by the GSTC:

Existing taxes are proposed to be subsumed under GST:

The GST would replace the following taxes:

Taxes currently levied and collected by the Centre:

a. Central Excise duty

b. Duties of Excise (Medicinal and Toilet Preparations)

c. Additional Duties of Excise (Goods of Special Importance)

d. Additional Duties of Excise (Textiles and Textile Products)

e. Additional Duties of Customs (commonly known as CVD)

f. Special Additional Duty of Customs (SAD)

g. Service Tax

h. Central Surcharges and Cesses so far as they relate to supply of goods and services

State taxes that would be subsumed under the GST are:

a. State VAT

b. Central Sales Tax

c. Luxury Tax

d. Entry Tax (all forms)

e. Entertainment and Amusement Tax (except when levied by the local bodies)

f. Taxes on advertisements

g. Purchase Tax

h. Taxes on lotteries, betting and gambling

i. State Surcharges and Cesses so far as they relate to supply of goods and services

Commodities kept outside the purview of GST:

Alcohol for human consumption, Petroleum Products viz. petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel and Electricity.

Types of GST to be implemented:

The GST to be levied by the Centre on intra-State supply of goods and / or services would be called the Central GST (CGST) and that to be levied by the States would be called the State GST (SGST). Similarly Integrated GST (IGST) will be levied and administered by Centre on every inter-state supply of goods and services.

Centre will levy and administer CGST & IGST while respective states will levy and administer SGST.

GST Rates:

The tax rates for different goods and services have been finalized. Besides, some goods and services would be under the list of exempt items.

The exempted services has been finalized which is same as the services exempted under existing service tax law, except services supplied by Goods and Services Tax Network which is the addition to the list of exempted services under service tax.

Rate for precious metals is an exception to ‘four-tax slab-rule’ and the same has been fixed at 3%.

A cess over the peak rate of 28% on certain specified luxury and demerit goods, like tobacco and tobacco products, pan masala, aerated waters, motor vehicles, would be imposed for a period of five years to compensate States for any revenue loss on account of implementation of GST.

81% of items to fall below/in 18% GST slab.

GST @ 0 %

GST @ 5%

GST @ 12%

GST@1 8%

Goods and Service Tax (GST) is a destination based tax on consumption of goods and services. It is proposed to be levied at all stages right from manufacture up to final consumption with credit of taxes paid at previous stages available as setoff. In a nutshell, only value addition will be taxed and burden of tax is to be borne by the final consumer.

Constitution (101st Amendment) Act, 2016

The Constitution (122nd Amendment) Bill was introduced in the 16th Lok Sabha on 19 December, 2014. The Bill was passed by the Lok Sabha in May, 2015.

The Bill with certain amendments was finally passed in the Rajya Sabha and thereafter by Lok Sabha in August, 2016.

Further the bill had been ratified by required number of States and received assent of the President on 8th September, 2016 and has since been enacted as Constitution (101stAmendment) Act, 2016 w.e.f. 16th September, 2016.

The levy of the tax can commence only after the GST Law has been enacted by all the legislatures. Four Laws namely CGST Act, UTGST Act, IGST Act and GST (Compensation to States) Act have been passed by the Parliament and since been notified on 12th April, 2017. The States have passed SGST Act.

Changes to the Constitution

Article 246A of the Constitution, which was introduced by the Constitution (101st Amendment) Act, 2016 confers concurrent powers to both parliament and state legislatures to make laws with respect to GST.

Under Article 269A of the Constitution, the GST on supplies in the course of inter-State trade or commerce shall be levied and collected by the Government of India and such tax shall be apportioned between the Union and the States in the manner as may be provided by Parliament by law on the recommendations of the Goods and Services Tax Council.

Goods and Services Tax Council (GSTC):

The GSTC has been notified with effect from 12th September, 2016. GSTC is being assisted by a Secretariat.

A Goods and Services Tax Council (GSTC) shall be comprised by the Union Finance Minister, the Minister of State (Revenue) and the State Finance Ministers to recommend on the GST rate, exemption and thresholds, taxes to be subsumed and other features.

One half of the total number of members of GSTC would form quorum in meetings of GSTC.

Decision in GSTC would be taken by a majority of not less than three-fourth of weighted votes cast. Centre and minimum of 20 States would be required for majority because Centre would have one-third weightage of the total votes cast and all the States taken together would have two-third of weightage of the total votes cast.

The following major decisions have been taken by the GSTC:

- The threshold exemption limit would be Rs. 20 lakh.

- For special category States enumerated in article 279A of the Constitution, threshold exemption limit has been fixed at Rs. 10 lakh.

- Composition threshold shall be Rs. 50 lakh. Composition scheme shall not be available to inter-State suppliers, service providers (except restaurant service) and specified category of manufacturers.

- Existing tax incentive schemes of Central or State governments may be continued by respective government by way of reimbursement through budgetary route. The schemes, in the present form, would not continue in GST.

- There would be four tax rates namely 5%, 12%, 18% and 28%.

Existing taxes are proposed to be subsumed under GST:

The GST would replace the following taxes:

Taxes currently levied and collected by the Centre:

a. Central Excise duty

b. Duties of Excise (Medicinal and Toilet Preparations)

c. Additional Duties of Excise (Goods of Special Importance)

d. Additional Duties of Excise (Textiles and Textile Products)

e. Additional Duties of Customs (commonly known as CVD)

f. Special Additional Duty of Customs (SAD)

g. Service Tax

h. Central Surcharges and Cesses so far as they relate to supply of goods and services

State taxes that would be subsumed under the GST are:

a. State VAT

b. Central Sales Tax

c. Luxury Tax

d. Entry Tax (all forms)

e. Entertainment and Amusement Tax (except when levied by the local bodies)

f. Taxes on advertisements

g. Purchase Tax

h. Taxes on lotteries, betting and gambling

i. State Surcharges and Cesses so far as they relate to supply of goods and services

Commodities kept outside the purview of GST:

Alcohol for human consumption, Petroleum Products viz. petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel and Electricity.

Types of GST to be implemented:

The GST to be levied by the Centre on intra-State supply of goods and / or services would be called the Central GST (CGST) and that to be levied by the States would be called the State GST (SGST). Similarly Integrated GST (IGST) will be levied and administered by Centre on every inter-state supply of goods and services.

Centre will levy and administer CGST & IGST while respective states will levy and administer SGST.

GST Rates:

The tax rates for different goods and services have been finalized. Besides, some goods and services would be under the list of exempt items.

The exempted services has been finalized which is same as the services exempted under existing service tax law, except services supplied by Goods and Services Tax Network which is the addition to the list of exempted services under service tax.

Rate for precious metals is an exception to ‘four-tax slab-rule’ and the same has been fixed at 3%.

A cess over the peak rate of 28% on certain specified luxury and demerit goods, like tobacco and tobacco products, pan masala, aerated waters, motor vehicles, would be imposed for a period of five years to compensate States for any revenue loss on account of implementation of GST.

81% of items to fall below/in 18% GST slab.

GST @ 0 %

- Unpacked Foodgrains

- Fresh Vegetables

- Unbranded Atta

- Unbranded Maida

- Unbranded Besan

- Milk

- Eggs

- Curd

- Lassi

- Unpacked Paneer

- Unbranded Natural Honey

- Jaggery

- Salt

- Kajal

- Phool Bhari Jhadoo

- Children's Drawing and Colouring Books

- Education Services

- Health Services

GST @ 5%

- Sugar

- Tea

- Roasted Coffee Beans

- Edible Oils

- Skimmed Milk

- Powder Milk

- Food for Babies

- Packed Paneer

- Cashew Nuts

- PDS Kerosene

- Domestic LPG

- Footwear (upto 500)

- Apparels (upto 1,000)

- Agarbatti

- Coir Mats

GST @ 12%

- Butter

- Ghee

- Almonds

- Fruit Juice

- Packed Coconut Water

- Preparations of Vegetables, Fruits, Nuts or other parts of Plants including Pickles

- Mobiles

GST@1 8%

- Hair Oil

- Toothpaste

- Soap

- Pasta

- Corn Flakes

- Soups

- Ice-cream

- Toiletries

- Computers

- H Printers

Published date : 03 Jul 2017 01:26PM