Sakshi Education

The wide range of applications envisioned for the consumer marketplace can be broadly classified into:

(i) Entertainment

(ii) Financial Services and Information

(iii) Essential Services

(iv) Education and Training

(i) Entertainment

(ii) Financial Services and Information

(iii) Essential Services

(iv) Education and Training

| Consumer Life-Style Needs | Complementary Multimedia Services | ||

| · · | Entertainment | Movies on demand, video cataloging, interactive Ads, Multi-user games, on-line discussions. | |

| · • | Financial Services and Financial news. | Home Banking, Financial services, Information, | |

| · • | Essential Services and remote diagnostics. | Home Shopping, Electronic Catalogs, telemedicine, | |

| · · | Education and Training conferencing, on-line databases. | Interactive education, multiuser games, video | |

- Personal Finance and Home Banking Management

(i) Basic Services

(ii) Intermediate Services

(iii)Advanced services

- Home Shopping

(i) Television-Based Shopping

(ii)Catalog-Based Shopping

- Home Entertainment

(i) Size of the Home Entertainment Market

(ii)Impact of the Home Entertainment on Traditional Industries

- Micro transactions of Information

- Personal Finance and Home Banking Management:

The newest technologies are direct deposit of payroll, on-line bill payment and telephone transfers. The technology for paying bills, whether by computer or telephone, is infinitely more sophisticated than anything on the market a few years ago. In 1980s were the days of “stone age” technology because of technology choices for accessing services were limited. For home banking, greater demands on consumers and expanding need for information, its services are often categorized as basic, intermediate and advanced.

(i) Basic services- These are related to personal finance

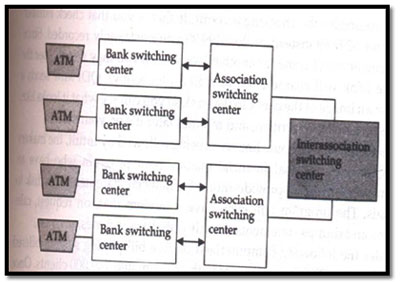

- The evolution of ATM machines from live tellers and now to home banking

- The ATM network has with banks and their associations being the routers and the ATM machines being the heterogeneous computers on the network.

- This interoperable network of ATMs has created an interface between customer and bank that changed the competitive dynamics of the industry. See in next figure

- Increased ATM usage and decrease in teller transactions

- The future of home banking lies with PC’s

Structure of ATM Network

Intermediate Services

The problem with home banking in 1980 is, it is expensive service that requires a PC, a modem and special software. As the equipment becomes less expensive and as bank offers broader services, home banking develops into a comprehensive package that could even include as insurance entertainment.

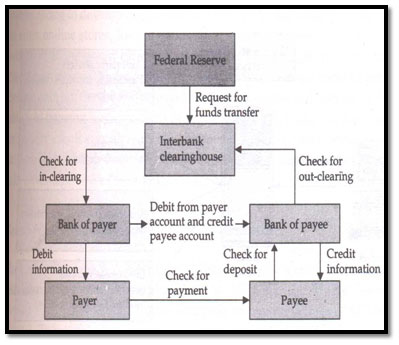

Consider the computerized on-line bill-payment system. It never forgets to record a payment and keeps track of user account number, name, amount and the date and we used to instruct with payment instructions. See in Fig;

Check-Clearing process

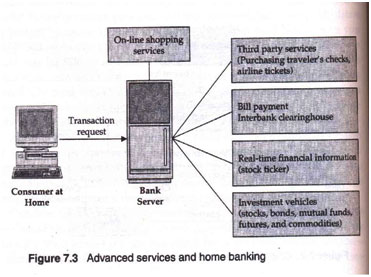

(iii)Advanced Services

The goal of advanced series is to offer their on-line customers a complete portfolio of life, home, and auto insurance along with mutual funds, pension plans, home financing, and other financial products. The Figure explains the range of services that may well be offered by banks in future. The services range from on-line shopping to real-time financial information from anywhere in the world. In short, home banking allows consumers to avoid long lines and gives flexibility

- Home Shopping:

It is already in wide use. This enables a customer to do online shopping

(i) Television-Based Shopping:

It is launched in 1977 by the Home Shopping Network (HSN). It provides a variety of goods ranging from collectibles, clothing, small electronics, house wares, jewelry, and computers. When HSN started in Florida in 1977, it mainly sold factory overruns and discontinued items. It works as; the customer uses her remote control at shop different channels with the touch of a button. At this time, cable shopping channels are not truly interactive

(ii) Catalog-Based Shopping- In this the customer identifies the various catalogs that fit certain parameters such as safety, price, and quality

- The on-line catalog business consists of brochures, CD-ROM catalogs, and on-line interactive catalogs

- Currently, we are using the electronic brochures

- Home Entertainment:

- It is another application for e-commerce

- Customer can watch movie, play games, on-screen catalogs, such as TV guide.

- In Home entertainment area, customer is the control over programming

Advanced Services

Size of the home Entertainment Market:- Entertainment services play a major role in e-commerce.

- This prediction is underscored by the changing trends in consumer behavior.

- It is shown in Table

Impact of Home entertainment on traditional industries:- This will have devastating effects on theater business

- Economic issues might allow theaters to maintain an important role in the movie industry

- Today average cable bill is approximately $30 a month Industry Estimates of consumer Expenditures

1980 ($4.7 bin)1990 ($31.0 bin)1993 ($37.8 bin)Theaters49.0% $2.314.5%$4.513.2%$5.0Basic cable35.0%$1.634.5%$10.736.9%$13.9Premium cable16.0%$0.816.5%$5.114.0%$5.3Home video____33.8%$10.534.8%$13.2Pay per view____0.7%$0.21.1%$0.4

- Micro transactions of information:

- One change in traditional business forced by the on-line information business is the creation of a new transaction category called small-fee transactions for micro services

- The customer by giving some information away for free and provide information bundles that cover the transaction overhead.

- The growth of small-money transfers could foster a boom in other complementary information services

- The complexity is also increased in micro services when an activity named, re-verification is entered.

- It means checking on the validity of the transaction after it has been approved

Desirable Characteristics of an Electronic marketplace- Critical mass of Buyers and sellers: To get critical mass, use electronic mechanisms

- Opportunity for independent evaluations and for customer dialogue and discussion: Users not only buy and sell products, they compare notes on who has the best products and whose prices are outrageous

- Negotiation and bargaining: Buyers and sellers need to able to haggle over conditions of mutual satisfaction, money, terms & conditions, delivery dates & evaluation criteria

- New products and services: Electronic marketplace is only support full information about new services

- Seamless interface: The trading is having pieces work together so that information can flow seamlessly

- Resource for disgruntled buyers: It provide for resolving disagreements by returning the product.

Mercantile Process models- Mercantile processes define interaction models between consumers and merchants for on-line commerce

Mercantile Models from the Consumer's Perspective

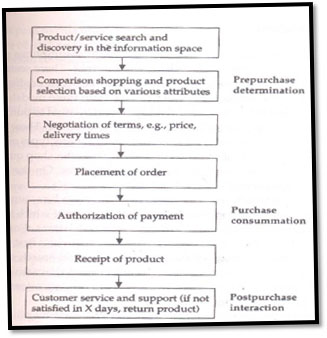

(i) Pre purchase preparation: The pre purchase preparation phase include search and discovery for a set of products to meet customer requirements

a. The consumer information search process.

b. The Organizational search process.

c. Consumer search experiences.

d. Information brokers & brokerages.

(ii) Purchase consummation: The purchase consummation phase includes mercantile protocols

a. Mercantile process using digital cash.

b. Mercantile transaction using credit cards.

c. Costs of electronic purchasing.

(iii) Post purchase interaction: The post purchase interaction phase includes customer service & support

Figure: Steps taken by a customer in product/service purchasing

(i) Pre purchase Preparation- The purchase is done by the buyers, so consumers can be categorized into 3 types

- Impulsive buyers, who purchase products quickly

- Patient buyers, purchase products after making some comparisons

- Analytical buyers, who do substantial research before making decision to purchase products.

Marketing researches have several types of purchasing:- Specifically planned purchases

- Generally planned purchases

- Reminder purchase

- Entirely unplanned purchases

The consumer information search process

Information search is defined as the degree of care, perception & effort directed toward obtaining data or information related to the decision problem.

The Organizational search process

Organizational search can be viewed as a process through which an organization adapts to such changes in its external environment as new suppliers, products, & services.

Consumer Search Experiences

The distinction between carrying out a shopping activity “to achieve a goal” (utilitarian) as opposed to doing it because “u love it”.

Information Brokers and Brokerages

To facilitate better consumer and organizational search, intermediaries called information brokers or brokerages. Information brokerages are needed for 3 reasons: Comparison shopping, reduced search costs, and integration

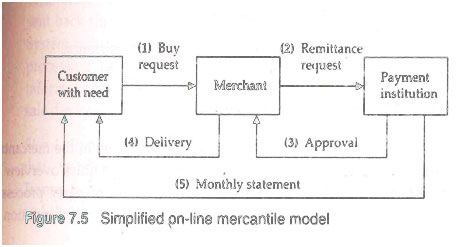

(ii) Purchase Consummation- Buyer contacts vendor to purchase

- Vendor states price

- Buyer and Vendor may or may not engage in negotiation

- If satisfied, buyer asks the payment to the vendor

- Vendor contacts billing service

- Billing service decrypts authorization and checks buyers account balance

- Billing service gives to the vendor to deliver product

- Vendor delivers the goods to buyer

- On receiving the goods, the buyer signs and delivers receipt

- At the end of the billing cycle, buyer receives a list of transactions

Mercantile process using Digital Cash- Buyer obtains e-cash from issuing bank

- Buyer contacts seller to purchase product

- Seller states price

- Buyer sends e-cash to seller

- Seller contacts his bank or billing service to verify the validity of the cash

- Bank gives okay signal

- Seller delivers the product to buyer

- Seller then tells bank to mark the e-cash as “used” currency

Mercantile Transactions Using Credit Cards

Two major components compromise credit card transactions in this process: electronic authorization and settlement

In retail transaction, a third-party processor (TPP) captures information at the point of sale, transmits the information to the credit card issuer for authorization, communicates a response to the merchant and electronically stores the information for settlement and reporting.

The benefits of electronic processing include the reduction in credit losses, lower merchant transaction costs, & faster consumer checkout & merchant-to-bank settlement

A step-by-step account of retail transaction follows:- Step1: A customer presents a credit card for payment at a retail location

- Step2: The point-of-sale software directs the transaction information to the local network

- Step3: System verifies the source of the transaction and routes it.

- Step4: In this, transaction count and financial totals are confirmed between the terminal and the network

- Step5: In this, the system gathers all completed batches and processes the data in preparation for settlement

A merchant client takes one of two forms:- Merchants are charged a flat fee per transaction for authorization and data capture services

- The other form of billing allows merchants to pay a ”bundled” price for authorization, data capture, & settlement

Cost of Electronic Purchasing:

Cash seems to be preferable to electronic payments, such as on-line debit, credit, and electronic check authorization. Consumers appear to spend more when using cards then when spending cash

(iii)Post purchase Interaction

Returns and claims are an important part of the purchasing process. Other complex customer service challenges arise in customized retailing are:

Inventory issues: To serve the customer properly, a company should inform a customer right away and if the item is in stock, a company must able to assign that piece to customer

Database access and compatibility issues: Customers should get kind of services by easy issues like calling an 800 number

Customer service issues: To clear the doubts of customer about product

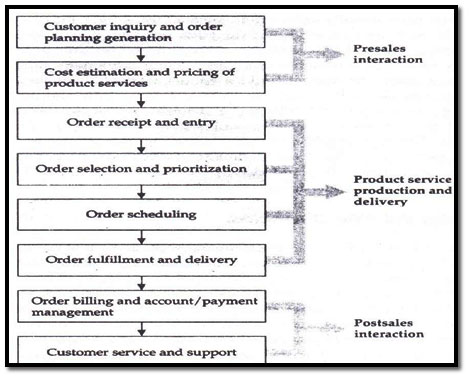

Mercantile Models from the Merchant's Perspective- To better understanding, it is necessary to examine the order management cycle (OMC).

- The OMC includes eight distinct activities.

- The actual details of OMC vary from industry to industry and also for individual products and services

- OMC has generic steps

(i) Order planning & Order generation.

(ii) Cost estimation & pricing.

(iii)Order receipt & entry.

(iv) Order selection & prioritization.

(v) Order Scheduling

(vi) Order fulfillment & delivery.

(vii) Order billing & account/payment management.

(viii)Post sales service.

Figure: Order management cycle in E- Commerce

Order planning & order Generation- Order planning leads to order generation.

- Orders are generated in a number of ways in the e-commerce environment.

- The sales force broadcasts ads (direct marketing), sends personalized e-mail to customers (cold calls), or creates a WWW page

Cost Estimation & pricing- Pricing is the bridge between customer needs & company capabilities.

- Pricing at the individual order level depends on understanding the value to the customer that is generated by each order, evaluating the cost of filling each order; & instituting a system that enables the company to price each order based on its value & cost

Order Receipt & Entry- After an acceptable price Quote, the customer enters the order receipt & entry phase of OMC.

- This was under the purview of departments variously titled customer service, order entry, the inside sales desk, or customer liaison.

Order Selection & Prioritization- Customer service representatives are also often responsible for choosing which orders to accept and which to decline.

- Not, all customers’ orders are created equal; some are better for the business.

Order Scheduling- In this phase, the prioritized orders get slotted into an actual production or operational sequence.

- This task is difficult because the different functional departments- sales, marketing, customer service, operations, or production- may have conflicting goals, compensation systems, & organizational imperatives:

Production people seek to minimize equipment changeovers while marketing & customer service reps argue for special service for special customers.

Order Fulfillment & Delivery- In this actual provision of the product or service is made.

- It involves multiple functions and locations.

Order Billing & Account/Payment Management- After the order has been fulfilled & delivered, billing is given by finance staff.

- The billing function is designed to serve the needs and interests of the company, not the customer.

Post sales Service- This phase plays an increasingly important role in all elements of a company’s profit equation: customer, price, & cost.

- It can include such elements as physical installation of a product, repair & maintenance, customer training, equipment upgrading & disposal.

Published date : 18 Jul 2015 03:09PM